KopenTech CLO Weekly: BWIC Activity & Market Trends, May 25 – May 29, 2026

June 01, 2026

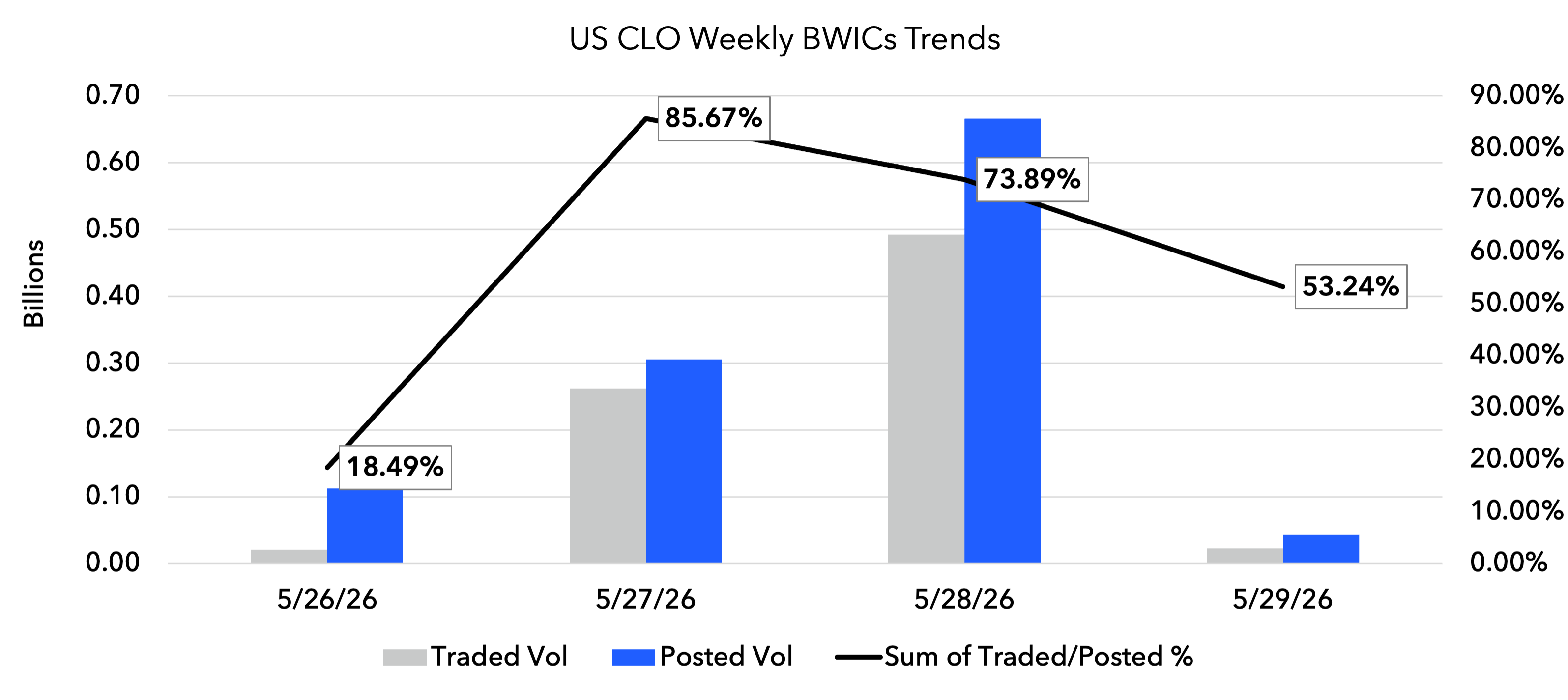

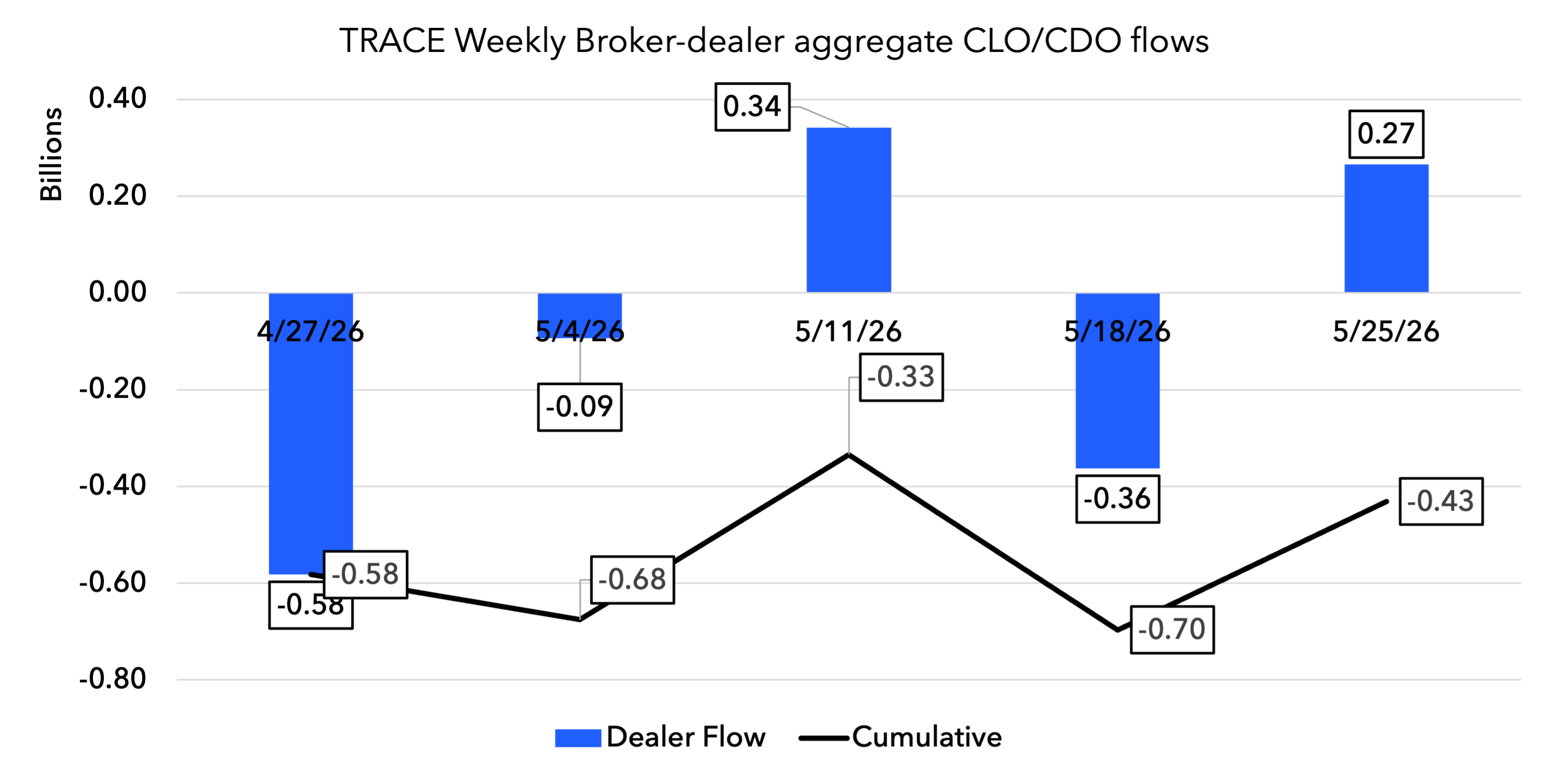

Secondary activity was compressed into four sessions following the Memorial Day holiday, yet the week delivered a tone that was meaningfully more constructive than its predecessor — conviction firmed, the bid broadened, and conversion rates ran well above recent levels. Against total posted volume of $1,126.7mm, $797.3mm cleared across 84 BWIC lists at a 70.8% conversion rate — flat in absolute traded dollars versus the prior five-day week, implying a materially stronger per-session pace. Tuesday and Wednesday anchored the week, accounting for over 94% of flow, while Monday's post-holiday re-open was tentative and Thursday tailed off predictably as the week compressed to a close. Dealer positioning reinforced the shift: the week of May 25 saw net buying of +$265.6mm, a sharp reversal from the -$362.8mm of net selling recorded the prior week.

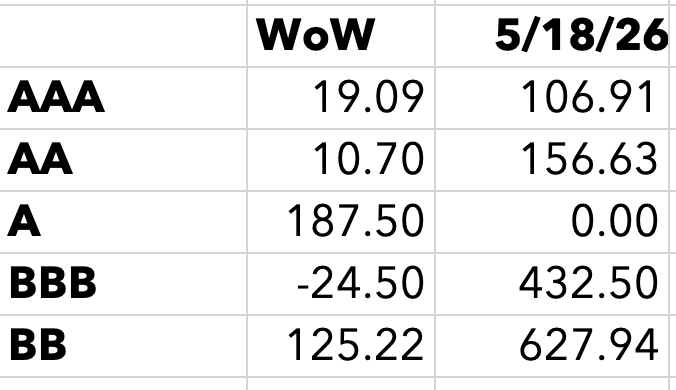

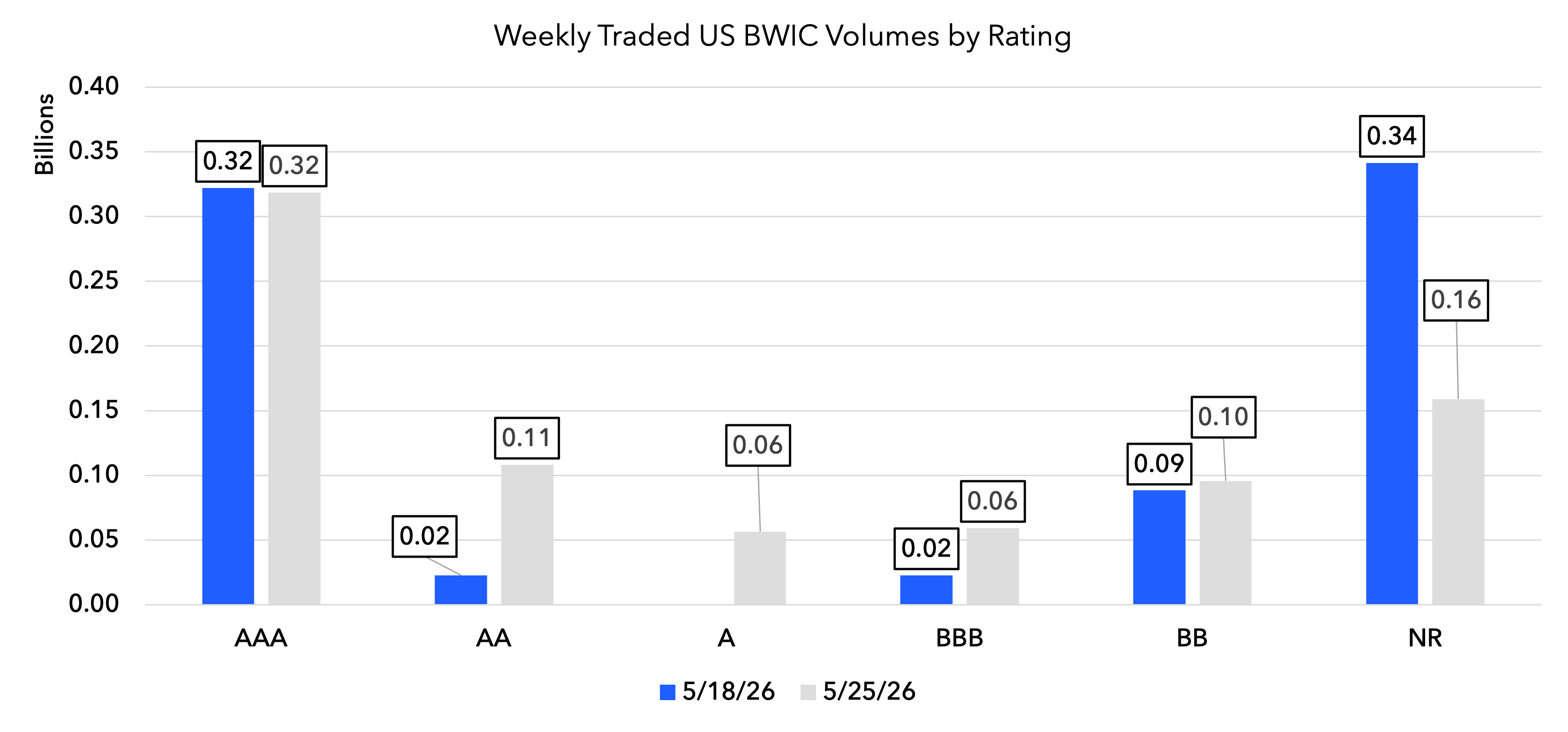

The capital stack told a story of deliberate rotation. AAA held its dominant share at 40.0% of traded volume ($318.7mm, effectively unchanged WoW in dollar terms), while IG mezzanine re-engaged sharply — AA surged from 2.9% to 13.6% of flow ($108.2mm) and single-A printed $56.5mm against zero the prior week, the strongest combined IG-mezz participation in recent weeks. BBB spreads tightened 24.5bps to 408bps DM as that part of the stack absorbed well. The notable outlier was BB, where average clearing DM widened 125bps to 753bps despite volume growing modestly — pointing to tiering and selectivity below the IG threshold rather than a broad risk-on move. Equity share contracted sharply from 42.8% to 19.9%, and the 849bps average DM compression in that bucket reflects a compositional shift toward cleaner paper rather than outright spread tightening. Into June, the tone is cautiously firmer at the top of the stack, with junior mezz and sub-IG remaining the focal point for price discovery.

US BSL CLO DMs WoW, bps